GAB welcomes this post by John Chevis, a former member of the Australian Federal Police, former accountant, and current member of the Intelligent Systems for State and Societal Resilience Hub at the University of New South Wales. As John explains below, he and colleagues at South Wales have developed an AI tool for producing National Anti-Money Laundering Risk Assessments. They are looking for those interested either in using it to conduct an NRA or supporting its further development. John and team can be reached at j.chevis@unsw.edu.au or johnchevis1@gmail.com

Using Artificial Intelligence to comply with the Financial Action Task Force’s directive to conduct a National Risk Assessment – an exercise to “identify, assess, and understand the money laundering and terrorist financing risks” member states face – would seem obvious.

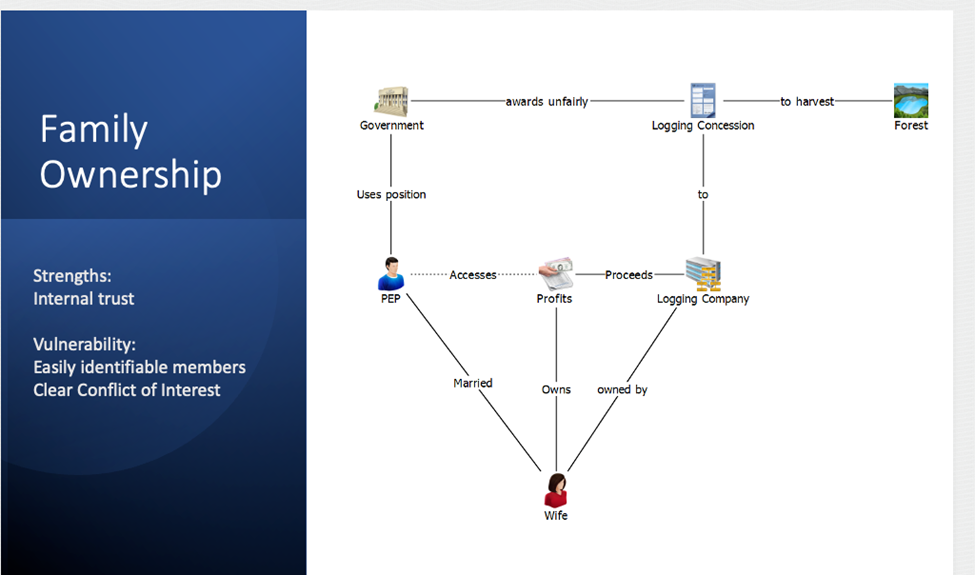

Financial Intelligence Units collect thousands, in larger countries millions, of reports banks and financial institutions submit about possible money laundering by customers. But a database of what is variously termed Suspicious Transaction or Suspicious Matter or Suspicious Activity Reports is by no means the only source for determining the money laundering risks a nation is exposed to. Other databases with millions of potentially useful records include those on cash transactions, company ownership, land titles, court cases, police investigations, and Politically Exposed Persons. There are also media accounts and social media posts. All grist for an NRA mill.

That’s where AI in the form of Large Language Models comes in. An LLM can sort through massive, unstructured datasets to identify patterns, trends, and anomalies, extracting relationships that human analysts with the most advanced mathematic tools might take years to spot — if ever. When brought to bear on data available to an FIU, the resulting analysis will not only highlight vulnerabilities in the nation’s anti-money laundering regime but provide investigative leads for law enforcement. Precisely the objectives of a National Risk Assessment.

Despite the obvious value of turning an LLM loose on FIU data, our team at the University of New South Wales is, to our knowledge, the first to apply AI to producing an effective digital National Risk Assessment. Funded by the Australian Department of Foreign Affairs and built for the Papua New Guinea financial intelligence unit, it is called “Neon.” Here is how it works.

Continue reading